Recovery Auditing 101: What It Is, What It Isn’t, and Why It Still Matters Today

Add bookmark

In an ever-changing world shaped by rapid advances in technology and AI, increasing ERP complexity, expanding regulatory requirements, and the growing adoption of e-invoicing, finance and shared services leaders face mounting pressure to stay ahead. Add that to multiple ERP systems, evolving operating models, and global cultures, and even best-in-class organizations can struggle to maintain full visibility and control across the Procure-to-Pay (P2P) lifecycle.

Despite these advances, many organizations still struggle with a less visible problem: value that quietly leaks out of the Procure-to-Pay process.

With so much focus on automation, transformation, and efficiency, it's fair to ask: Where does recovery auditing fit in today, and does it still matter in modern P2P environments?

The short answer is yes. When positioned correctly, recovery auditing plays a critical role in protecting value, strengthening controls, and validating that investments in people, process, and technology are delivering the intended results.

What Is Recovery Auditing?

At its core, recovery auditing is a structured review of accounts payable (AP) and procurement activity designed to identify and recover funds paid in error or never realized in the first place. These issues are rarely the result of negligence. More often, they stem from the sheer volume and complexity of modern P2P environments.

In large organizations, the financial impact can be substantial. Fortune 500 companies frequently recover $10 million or more in the first year of a structured recovery program, with additional recoveries continuing year over year as new exceptions surface.

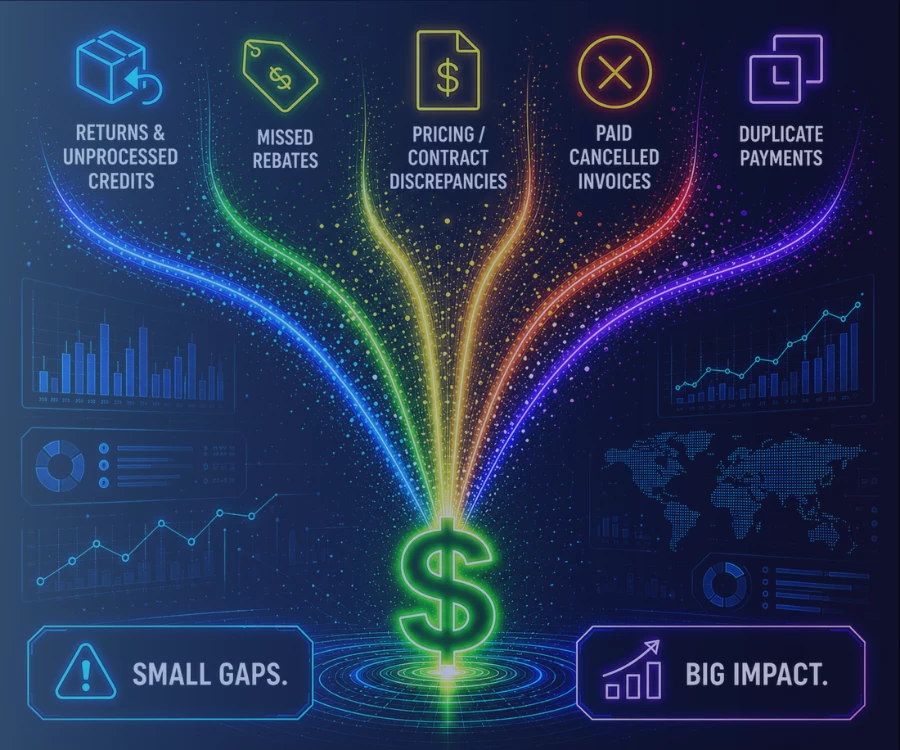

Common recovery areas include:

- Duplicate or erroneous payments

- Paid cancelled invoices

- Missed or unapplied vendor credits

- Pricing or quantity discrepancies

- Uncaptured vendor rebates

- Debit balances and unrealized credits

Importantly, recovery auditing is not about blame. It is about visibility. Even highly automated environments generate exceptions, and recovery reviews provide a disciplined way to surface and resolve them.

What Recovery Auditing Isn't

Recovery auditing is often misunderstood, which has given it an unfair reputation in some organizations.

- It is not about creating new value through increased sales or growth initiatives.

- It is not about cutting headcount or reducing investment in critical processes.

- And it should not be an adversarial exercise that damages supplier relationships.

Recovery auditing is not a process driven by competing priorities or conflicting incentives. Instead, it should center on recovering funds, strengthening processes and communication, and supporting broader business objectives.

At its core, recovery auditing focuses on reclaiming value that already belongs to the organization, funds that slipped through due to timing differences, system limitations, data gaps, or process handoffs that did not work as designed.

When recovery is embedded into the P2P framework, it becomes less about "finding mistakes" and more about ensuring completeness and accuracy across the lifecycle.

Why Recovery Auditing Still Matters - Even in Advanced Environments

One of the most common questions from finance leaders is:

"If we have modern ERPs, automation, and analytics, why do we still need recovery auditing?"

The answer lies in reality.

Automation reduces errors, but it does not eliminate them. Systems are only as good as the data, configurations, and governance behind them. Supplier behavior changes. Contracts evolve. Mergers, divestitures, and reorganizations introduce complexity. As organizations scale, small exceptions can quietly accumulate into material dollars.

Recovery auditing acts as the final validation layer, confirming that upstream controls, sourcing strategies, and payment processes are working as intended.

How Recovery Auditing Fits into a GBS Model

Within a Global Business Services (GBS) organization, recovery auditing fits naturally and powerfully.

Think of it as the tail-end quality assurance function of the Procure-to-Pay lifecycle. A structured recovery program not only recovers funds that impact the bottom line but also provides insight into where breakdowns occur across functional boundaries.

For example:

A well-negotiated rebate by Procurement that never reaches Accounts Payable

Supplier credits that remain unapplied due to missing PO numbers, multiple PO references, or non-PO transactions

Credits that become cancelled or obsolete when ownership or approval paths break down between Procurement and Accounts Payable

Utilities or services tied to closed locations that continue to bill incorrectly

An in-house recovery capability within GBS provides centralized visibility across these touchpoints, reinforcing communication between Procurement, AP, Finance, and Operations. The result is not just recovered dollars, but process insight that strengthens the entire operating model.

In-House Recovery: Building Control and Institutional Capability

Recovery auditing has traditionally been performed by external specialists, but many organizations are recognizing the advantages of developing recovery capabilities internally.

When recovery is built in-house, it becomes an embedded capability within the operating model. Internal teams gain deeper visibility into supplier behavior, contract execution, system configurations, and process handoffs across the P2P lifecycle.

Just as importantly, the knowledge gained through recovery work remains within the organization. Teams build expertise, strengthen cross-functional collaboration, and develop a clearer understanding of where breakdowns occur and how to prevent them.

An in-house recovery capability also provides greater control over sensitive financial data, supplier interactions, and process governance. Organizations retain direct ownership of both the recovery process and the operational improvements that follow.

Final Thought

Recovery auditing is not a relic of the past. It is a relevant discipline that complements automation, supports working capital objectives, and validates the effectiveness of today's complex P2P environments.

When positioned correctly, particularly within an in-house, GBS-aligned model, recovery auditing becomes less about looking backward and more about protecting value, validating processes, and reinforcing financial control going forward.